FRACTIONAL INTERESTS

Fractional Interests

This content is intended for general informational purposes only and should not be construed as tax, legal, or financial advice.

Fractional Interests, also known as Undivided Interest or Co-Ownership, provide a means to own smaller portions of a larger whole. These fractional interests hold particular significance in the realm of real estate, especially in the context of 1031 tax deferred exchanges. This significance arises due to the application of the Same Taxpayer Rule and the Like Kind Rule within the tax code.

The rationale behind these fractional interests is the prevention of scenarios where an exchanger sells a single-family rental property and attempts to exchange it for an LLC interest in a Multifamily syndication. This is not possible because shares of an LLC are categorized as personal property rather than real property, thus leading to the disqualification of the Like Kind Rule. Additionally, an LLC represents a distinct taxpayer and tax structure, thereby altering the tax status of the exchanger and disqualifying the Same Taxpayer Rule. To adhere to these rules and maintain the validity of a 1031 Exchange, fractional interest or co-ownership arrangements come into play. Here are the primary methods through which they are achieved.

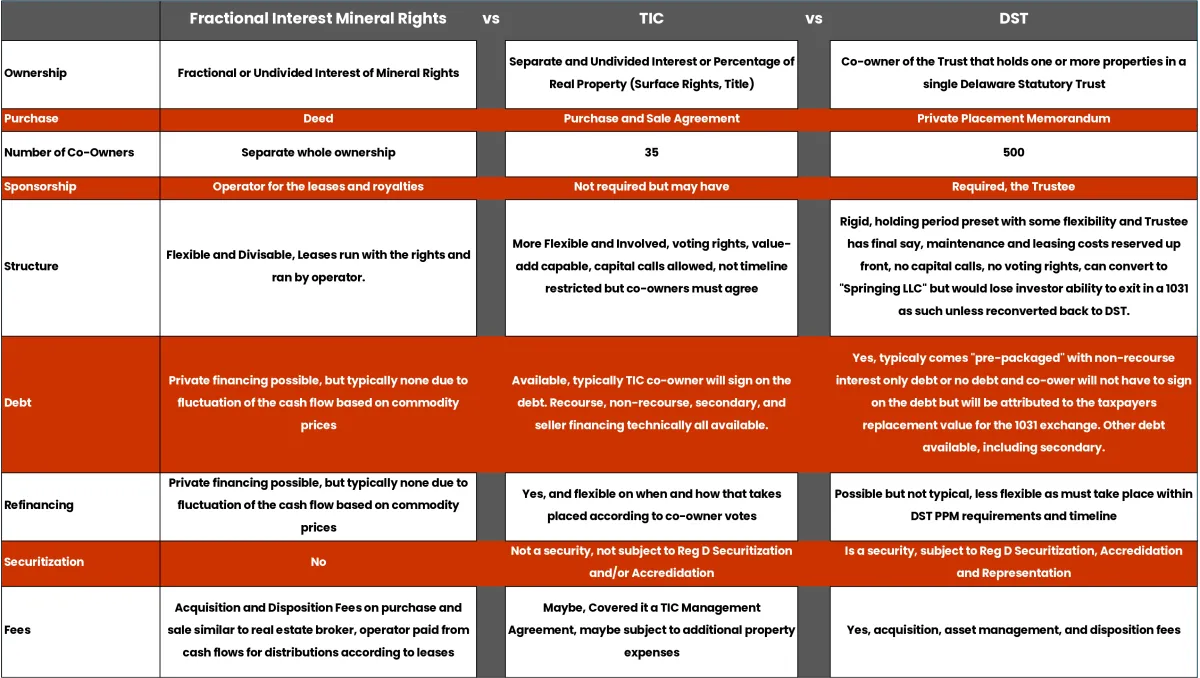

Fractional or Undivided Mineral Interest

Mineral Rights are categorized as Real Property and meet the requirements of the Like Kind Rule for 1031 Exchanges. These rights confer the authority to extract and sell minerals found beneath the earth's surface, such as gold, silver, copper, oil, natural gas, and coal. The subdivision of mineral rights into fractional interests satisfies the Same Taxpayer Rule, making oil & gas royalties eligible for a 1031 Exchange. Notably, mineral rights are distinct from surface rights, which encompass forms of real estate ownership familiar to investors and property owners like Fee Simple Interest, Leasehold, and Ground Lease. These forms also qualify for a 1031 exchange, given certain conditions are met, and they can be subdivided into fractional interests as well. This is typically achieved through Tenancy in Common and Delaware Statutory Trusts.

Tenants-in-common (TIC)

Tenants-in-common (TIC) primarily function as a title structure that enables multiple owners to collectively buy, maintain, and sell equity in real property through standard purchase and sale agreements. Ownership is registered as separate and undivided interests on the title. For instance, a title report might indicate that ABC LLC owns 12.5%, DEF LLC owns 7.5%, and XYZ LLC owns 80% of 123 Main St. New York, New York 12345. TICs offer flexibility in dividing ownership percentages among members to fulfill 1031 exchange replacement value requirements. However, co-owners must sign purchase and sale agreements during property transactions and assume responsibility for any property-related debt. TICs are limited to 35 co-owners, and each owner receives an individual profit and loss statement. While the entire TIC isn't taxed as a partnership, individual owners are treated as taxpayers who purchased the property. TICs involve voting rights, and a TIC Management Agreement is often used to allocate responsibilities and fees to a property manager who makes decisions regarding property management, sales, refinancing, etc. An investor need not be accredited to participate in Tenants in Common. It's possible to divide a small duplex or single-tenant net lease property through TIC and engage in a 1031 exchange with smaller investments. For larger deals, a sponsor purchasing a multifamily or distribution center property can bring in Tenants in Common for co-ownership with varying investment amounts.

Delaware Statutory Trust (DST)

A Delaware Statutory Trust involves the ownership of one or multiple properties by a single entity, often with a master lease, which is then enveloped by the DST. Once incorporated into a Delaware Statutory Trust, the investment can be funded through cash or 1031 exchange funds, resulting in shares of the DST. A single DST can accommodate over 500 investors, allowing for a broader investment base with relatively smaller contributions, sometimes as low as five figures and less than 1% of the DST's value. If the DST has any debts, they are often non-recourse, eliminating the need to assume any loans while still satisfying the full replacement value required for a successful 1031 exchange. Delaware Statutory Trusts are considered securities, requiring both investors and exchangers to be accredited and to go through a broker-dealer while signing a private placement memorandum to secure their shares. DSTs are categorized as illiquid assets, and shares cannot be bought or sold during the DST's active course, as decisions are made by the DST's trustee. DST sponsors, who may be trustees of real estate investment trusts, can also provide a 721 Exchange or UPREIT option at the end of the DST's term as the properties within are absorbed into the REIT.

Fractional Interest Mineral Rights vs TIC vs DST

In summary, these options offer ways to purchase smaller segments of a whole while satisfying the Like Kind and Same Taxpayer Rules of the 1031 Exchange. Each option has its own set of advantages and drawbacks, contingent on the investor's risk tolerance, strategy, and objectives. It's important to note that not all fractional interest opportunities are continuously available. Depending on the taxpayer's 1031 exchange timeline, they may consider only options that align with their individual schedule. Identifying available options before executing a 1031 exchange is crucial to reserving percentages and shares in advance, ensuring a successful tax deferral.

Office: Atlanta, Georgia

Call 470-387-1031

Email:nathan@aea1031.com

Site: www.aea1031.com